Zillow released its Q1, 2022 iBuyer report a few days ago and well, it was kind of drowned out by the CPI print and the ensuing market collapse, including mortgages going over 6%. There are some interesting things in the report, but I have a simple and quick question. And it’s not a rhetorical question; I honestly don’t know the answer.

What’s the tipping point where iBuyer services become mainstream?

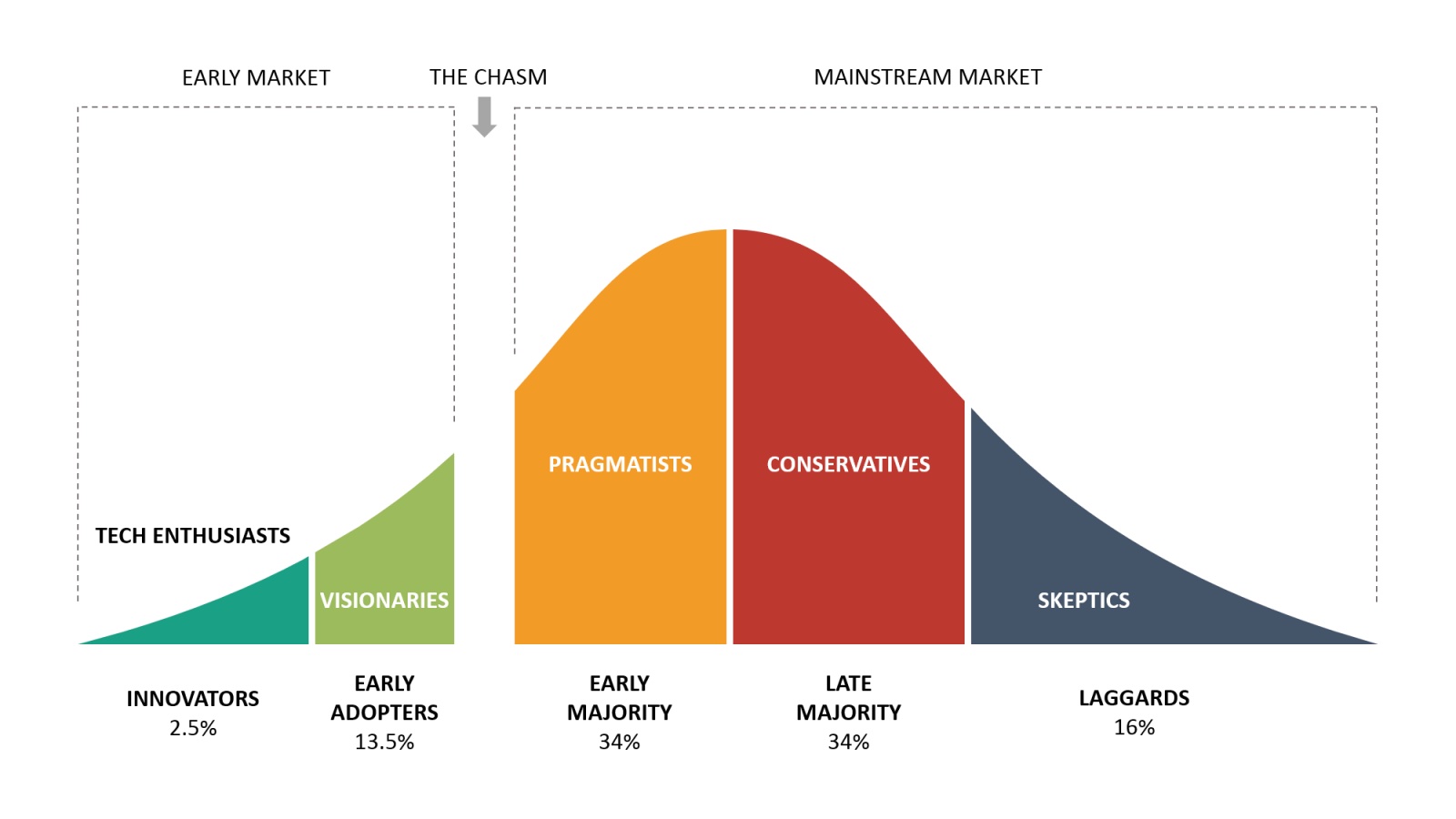

In Geoffrey Moore’s classic work, Crossing the Chasm, we get introduced to the technology adoption lifecycle and different groups of consumers. New technologies must figure out how to move from Innovators and Early Adopters into the mainstream. That difficult jump from a fad or curiosity to mainstream acceptance is crossing the chasm. From ThinkInsights:

Think Insights thinks the divisions are standard deviations from the median, so the first 2.5% are Innovators, then the next 13.5% are the Early Adopters. You then have to cross the chasm and become accepted by the Early Majority, which make up 34%. So basically, until you hit somewhere around 16% market share, you’re not ready for the chasm at all.

Think Insights thinks the divisions are standard deviations from the median, so the first 2.5% are Innovators, then the next 13.5% are the Early Adopters. You then have to cross the chasm and become accepted by the Early Majority, which make up 34%. So basically, until you hit somewhere around 16% market share, you’re not ready for the chasm at all.

iBuying and the Chasm

According to Zillow iBuying nationally in Q1 of 2022 had 1.3% market share in terms of people selling to iBuyers, down from 1.7%. Even in Tucson, AZ which had the highest market share for selling to iBuyers, that figure was only 6.1%. Nationally, iBuying is still in the Innovators phase. In some markets, we’ve moved into Early Adopters.

However… Zillow includes a very nice table (go check it out yourself) which shows that the 1.3% market share number comes from iBuyer Purchases (i.e., the iBuyer acquires a house from a homeowner) of 12,652. Thankfully, Zillow also includes iBuyer Resales, that is when the iBuyer is acting as the seller. That number is 26,537… which is just about double home purchases. So let’s call that 2.6% market share for Resale? Combined, we’re at 4% — past the Innovators and well into Early Adopters.

Thing is, those are national numbers. And iBuyers are only in a few dozen markets and completely absent from some of the highest population markets like New York, Chicago, etc. It feels like using national market share numbers would undercount the impact of iBuying on the relevant consumer psychology.

So let’s take some of the top iBuying markets.

| Market | Homes Purchased | Market Share | Homes Resold | Market Share? | Combined |

| Q1/2022 | |||||

| Atlanta, GA | 1,628 | 6.00% | 3,302 | 12.17% | 18.17% |

| Phoenix, AZ | 1,232 | 5.20% | 3,040 | 12.83% | 18.03% |

| DFW, TX | 1,116 | 5.10% | 2,043 | 9.34% | 14.44% |

| Houston, TX | 844 | 3.50% | 1,562 | 6.48% | 9.98% |

| Charlotte, NC | 612 | 5.60% | 1,439 | 13.17% | 18.77% |

| Q4/2021 | |||||

| Atlanta, GA | 2,925 | 9.60% | 2,652 | 8.70% | 18.30% |

| Phoenix, AZ | 2,324 | 8.80% | 2,404 | 9.10% | 17.90% |

| DFW, TX | 1,655 | 5.80% | 2,064 | 7.23% | 13.03% |

| Houston, TX | 1,199 | 4.40% | 1,241 | 4.55% | 8.95% |

| Charlotte, NC | 1,228 | 8.50% | 1,195 | 8.27% | 16.77% |

I have to estimate what the market share of the Homes Resold is, since Zillow doesn’t give that to us. But I reason that Sales and Purchases have to be the same since each home changing hands has two transaction sides. With the time lag, that might not be correct, but I figure it’s good enough for government work and for short blogposts.

The point is that if you combine consumers who sold to an iBuyer with consumers who bought from an iBuyer, we suddenly get to percentages that look much, much closer to crossing the chasm. In Atlanta, we’re potentially looking at 18% of consumers interacting with an iBuyer either as a seller, or as a buyer. We’re at the chasm, and possibly across it.

So what do we think the tipping point for iBuying is, where it ceases to be an exotic oddity and much more accepted as a mainstream transaction method? If we go by Crossing the Chasm, then we’re already there in some of the top iBuying markets. If we think the number is higher, then what do you think that is? 25% of consumers? 30%?

Comment below with your tipping point threshold.

-rsh